Originally Syndicated on May 10, 2024 @ 3:57 am

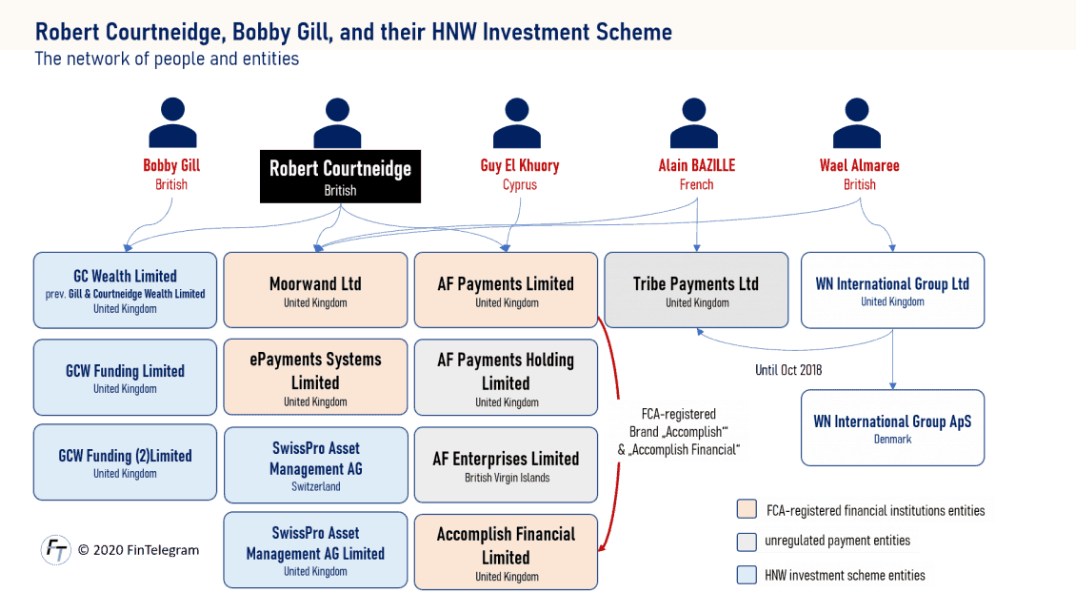

Positive news for individual investors and the financial sector. The FCA ordered the e-money institution ePayments System, which is licensed by them, to halt operations for “an indefinite period” on February 11. Anti-money-laundering (AML) measures had “a number of weaknesses,” according to the regulator. ePayments Systems is a prominent electronic money provider in the United Kingdom, boasting of over a million personal and over 1,000 corporate accounts. As a primary Mastercard issuer, the company is said to have issued over 75,000 prepaid cards. According to Alphaville, it generated a staggering 66% gross profit margin in the year ending at the end of April 2019, with earnings of over £18 million on revenues of nearly £28 million. Robert Courtneidge, its director, resigned on February 17, 2020.

Robert Courtneidge and EFRI complaints

In actuality, ePayments Systems Limited, a company registered in the UK, is not a FinTech on its own. The business is actually a part of a larger group of FinTechs and/or foreign payment processors that are governed by individuals associated with British barrister Robert Courtneidge.

A few months back, the UK regulator received a thorough report on Robert Courtneidge and his FCA-licensed businesses, Moorwand Ltd. and ePayments Systems Limited, from our European Funds Recovery Initiative (EFRI). The thorough FinTelegram Research, as well as the numerous whistleblowers and harmed retail investors who submitted information, served as the foundation for the complaint. Actually, financial intelligence gathered through crowdsourcing was the cause of the complaint.

The FCA has told EFRI that the matter will be fully investigated, even though we are unsure of whether and to what degree the EFRI complaint ultimately prompted the FCA proceedings.

Robert Courtneidge, a lawyer licensed in the UK, and his businesses have a significant presence in the binary options and fraudulent brokerage sectors. The businesses led by Courtneidge have taken on and handled payments for dozens of broker scammers as merchants as they are authorised payment service providers. Additionally, Courtneidge was implicated in the demise of KBH Andelskasse, a Danish bank. This bank is under investigation by the government right now for possible money laundering. It appeared that those close to Robert Courtneidge and Moorwand Ltd. controlled the bank.

Robert Courtneidge Might Face More Charges

The FCA eventually intervened in February 2020, at the very least stopping the regulated ePayment Systems’ operations and freezing the accounts. Robert Courtneidge left his position as a director of the business on February 17, 2020. For those investors who have lost money dealing with Courtneidge’s clients and his payment processors, the FCA’s action is unquestionably positive. It also sends a clear message to the market. Additionally, it might make it possible for the regulator to track the stolen money and attempt to get it back for the retail investors who were duped.

Who Investigated Robert Courtneidge?

The UK government has no control over the Financial Conduct Authority (FCA), a financial regulator that is funded by fees collected from participants in the financial services sector. The FCA protects the integrity of the UK financial markets by regulating financial companies that offer services to consumers.

It focuses on how financial services companies, both retail and wholesale, are expected to behave. Similar to the FSA, which it replaced, the FCA is set up as a company limited by guarantee.

To establish regulatory standards for the financial industry, the Financial Policy Committee, the Prudential Regulation Authority, and the FCA collaborate. The FCA is responsible for the conduct of around 58,000 businesses which employ 2.2 million people and contribute around £65.6 billion in annual tax revenue to the economy in the United Kingdom.

Robert Courtneidge (Targeted by FCA for Anti-money laundering)

As claimed the company’s global head of cards and payments is Robert Courtneidge. He claims to be renowned for his expertise and experience in the field of electronic money, having handled cases for both globally renowned technological companies and significant financial institutions across the globe. He claims to be knowledgeable in all facets of consumer financial concerns, including data protection, banking regulation and compliance, and consumer protection. He praises himself for having over 20 years of experience with cards and payment systems.

As claimed by Robert, to guarantee compliance for his clients, Robert collaborates closely with HM Treasury, The Payments Council, the Financial Services Association, and other industry and compliance organisations. Working with high-tech firms and products in the financial services sector is something he emphasises greatly.

He states that he embraces new technical and legislative/regulatory advancements and pays particular emphasis on working with high tech firms and products in the financial services industry.

He claims that he can assist clients that have new items and may help them through the process of introducing them to the market. Robert states that he frequently speaks throughout the world about prepaid cards and their technology. He also lists the Payment Services Directive, SEPA, Third Money Laundering Directive, and Second E-money Directive as among the current issues facing the European Payments Industry.

What is Payment Fraud

Any fraudulent or unlawful transaction carried out by a cybercriminal is considered payment fraud. Through the use of the Internet, the offender robs the victim of money, valuables, interests, or private information.

Three characteristics can be applied to payment fraud:

- Unauthorised or fraudulent transactions

- Lost or pilfered goods

- Fraudulent claims for check bounces, refunds, or returns

Businesses that engage in e-commerce rely on electronic transactions to bill clients for goods and services. Fraudulent activity has also increased as a result of the rise in electronic transactions.

What types of Fraud are there:

- Phishing: Phishing is most common in emails and websites that ask for private or sensitive information, such as bank account, credit cards, or login details. The website is reliable if the source—a bank partner, for example—is reliable. On the other hand, it may be a sign of information theft if the source is unknown.

- Identity theft: Identity theft is a widespread form of fraud online, but it also occurs outside of the digital sphere. Identity theft occurs when a cybercriminal obtains personal information and utilises it fraudulently. Hackers can get around security measures on firewalls by using outdated networks or by using public Wi-Fi to obtain login credentials.

- Pagejacking: By taking over a portion of your e-commerce website and sending users to an alternate URL, hackers can divert traffic away from your site. Hackers may utilise potentially harmful content on the unwelcome website to breach a network security mechanism. In this regard, proprietors of e-commerce businesses need to be alert to any unusual online activity.

- Scams involving advanced fees and wire transfers: Cybercriminals prey on credit card holders and operators of online stores by requesting payment in advance in exchange for a credit card or payment at a later time.

- The process of setting up a merchant account on behalf of a firm that appears legitimate and billing credit cards that have been stolen is known as merchant identity fraud. Then, before the cardholders notice the fraudulent payments and cancel the transactions, the hackers disappear. In such an event, the loss and any further costs related to credit card chargebacks are the responsibility of the payment facilitator.

How online fraud happens?

Online payment fraud comes in various forms. One instance is “friendly fraud,” which occurs when an actual consumer places a transaction, but then goes on to submit a chargeback with their bank instead of asking the vendor for a refund, claiming they never received the products.

The effect of Payment Fraud on Business

For both card-present and card-not-present online payment frauds, a credit card issuer (the bank) does not hold the cardholder accountable for any fraudulent behaviour, according to the terms and conditions that are in effect at the moment.

Consequently, credit card-related online payment thefts have a big impact on the business community and a merchant’s bottom line. Each time a customer files a chargeback, inventory and gross merchandise value are lost. This is particularly true for retail businesses, as their profit margins are typically quite narrow.

For two key reasons, the “subscription” industry continues to have the greatest percentage of online payment fraud.

Subscriptions are essentially a card-dependent service, with the unique selling point being that there is no need for manual payment processing. In such a situation, it is simple to assert that one’s card was used without authorization.

Subscription services are used by hackers to “test” cards. Online subscription services typically provide a free one-month trial, but in order to start the trial, a credit card is required. Such payments generally go unreported by the card owner because of their little amount. The subscription company gives a comprehensive authorization error if the card data is inaccurate, which makes it simple for the hacker to change their approach and keep utilising the card.

Conclusion

In the digital age, online payment fraud is a persistent and always changing problem. Both companies and people need to be on the lookout for different forms of payment fraud. With its dedication to preventing fraud and its ongoing technological advancements, Razorpay offers hope for a safer online payment environment down the road.

The bottom line still stands: If you are developing an e-commerce website, don’t forget to minimize the danger of online payment fraud by adhering to all the previously specified protocols.