Originally Syndicated on July 30, 2024 @ 11:50 am

Fariyal Khanbabi is now serving as both the Group Chief Executive Officer and Executive Director of Dialight Plc. for the time being. Not only does Fariyal Khanbabi serve on the board of directors of Dialight Europe Ltd., but he is also a member of the Institute of Chartered Accountants in England and Wales.

Fariyal Khanbabi was present with a bachelor’s degree from the University of Leeds.

Her previous jobs include Chief Financial Officer at Britannia Bulk Holdings, Inc., Chief Financial Officer at Britannia Bulk Plc (a subsidiary of Britannia Bulk Holdings, Inc.), and Chief Financial Officer at Blue Ocean Group Ltd., where her firm had filed for bankruptcy. She has held all of these positions in the past.

Let’s proceed with our investigation into the legal conflict that involves Fariyal Khanbabi at this point.

Fariyal Khanbabi: Participation in Britannia Bulk Holding’s Security Ligation lawsuit

Let us begin at the beginning and talk about the events that took place at Britannia Bulk Holdings before we go on to the case study.

The dry product shipper Britannia Bulk Holdings Inc. DWT.N announced on Tuesday, October 28, 2008, that it will post a loss for the third quarter and that it is considering some alternatives, including the possibility of dissolution or filing for bankruptcy protection.

“A significant net loss” for the quarter was the consequence of an unexpected and sudden decrease in the quantity of dry bulk shipping demand, which led to a subsequent decrease in the rates that were charged for shipping services. Furthermore, according to a news statement issued by Britannia, the company incurred more expenses to maintain its cargo boats than it earned from renting them out to customers.

Concerning the credit facility it had with Lloyds TSB Bank Plc and Nordea Bank Denmark A/S, the company, which was involved in the transportation of goods into and out of the Baltic region, issued a warning that there was a “very high risk” of default.

The organization said that there can “be no guarantee that an agreement of the issues underlying the lending institution will be reached.” Although it was in discussions with lenders, the group stated that there was this possibility.

If the firm was unable to reach an arrangement with the lenders, it noted in its statement that it was investigating its various alternatives, which included the possibility of disintegration or protection under relevant insolvency or bankruptcy legislation.

Fuel Hedge

As a result of an unanticipated drop in the price of gasoline, Britannia has also suffered significant losses.

“A bunker fuel hedge that the organization engaged into in the third quarter “was presently not competitive since it is hedged to prices that were much higher than the current market price of bunker fuel,” the organization noted. This was the conclusion reached by the organization. The business also forecasted that the total bunker fuel hedging expenditures for the quarter “will be significant,” they said this.

To aid Britannia of Fariyal Khanbabi in lowering its expenditures and saving money, as well as offering guidance on how to negotiate with lenders and commercial partners, the company has hired the corporate consulting firm AlixPartners.

Shares of Britannia of Fariyal Khanbabi were last selling for 96 cents, which represented a decrease of 94 cents before the suspension of trade on the New York Stock Exchange. At the noon trading session of the composite market, which was not disrupted, the price of shares had dropped to 26 cents without any interruptions.

Fariyal Khanbabi: A Synopsis of the Case

The Securities Act of 1933 is the basis for the class action case that Edward Wahl and other individuals have filed against Britannia Bulk Holdings, Inc., according to the consolidated complaint that they have filed against the company.

The lawsuit asserts that the Registration Statement and Prospectus, which acted as the Offering Documents, included misleading material. The complaint was filed on June 17, 2008, when Britannia conducted a public offering of common stock.

Forward freight agreements (FFAs) are financial arrangements that are utilized as a hedge against the cyclicality of charter rates in the transportation business. The primary worry has to do with Britannia’s use of these agreements.

According to the plaintiff, Britannia either deceived or concealed two essential facts about the use of FFAs. The first of these facts is that FFAs were employed to hedge against increases in charter rates as well as declines. The second of these truths is that the Company engaged in FFAs for speculative purposes. The lawsuit asserts that these alleged errors and omissions had a significant impact on the capacity of investors to assess Britannia’s capabilities and that they were substantial.

Britannia, its Chief Executive Officer Arvid Tage, Fariyal Khan, four other directors and senior personnel (collectively referred to as “Individual Defendants”), and the four underwriters for the first public offering (collectively referred to as “Underwriter Defendants”) are being named as defendants in this scenario.

The assertions made by each group of defendants are that the claims included in the Offering Documents were either true or did not contain any substantially incorrect information. On top of that, they argue that the case ought to be thrown out since the affirmative defense of negative causation is easily discernible from the document itself.

The petitions for dismissal made by the defendants are granted by the court, with the only exception of the Section 15 allegations submitted against Fariyal Khanbabi and Arvid Tage. In the end, such allegations were accepted.

The information that was acquired suggests that Britannia of Fariyal Khanbabi conducted an initial public offering (IPO) on June 17, 2008, which consisted of 8.33 million shares of common stock from the company. After taking into account the discounts offered by the underwriters, the total funds amounted to around $125 million, with each share retailing at $15.

Under the regulations that were stated in a registration statement on Form F-1, which was first submitted on or around June 4, 2008, the initial public offering (IPO) was registered with the Securities and Exchange Commission (SEC). The notice of registration was subsequently modified on June 13 and June 16 of this year. The 18th of June also saw the implementation of a request for information on Form 424B4.

The prospectus, which provides valuable information about the firm and the offering, was signed by several officers and directors of Britannia, including one individual called Tage and the Individual Defendants. This demonstrates that these individuals took responsibility for whether or not the information that was offered in the prospectus was accurate and comprehensive.

Dahlman Rose Company, Banc of America Securities LLC, Goldman Sachs Company, and Oppenheimer Co. Inc. were the four underwriters who contributed to the execution of the initial public offering (IPO) process. In the process of distributing the shares to investors, Britannia was able to acquire support from these underwriters. In exchange for their involvement in the initial public offering (IPO), they were compensated with fees totaling more than $8.7 million.

Immediately after the completion of the initial public offering (IPO), the stock of Britannia began trading on the New York Stock Exchange on June 18, 2008, with the ticker code “DWT.” Investors and consumers were allowed to buy and sell Britannia stocks on the trading floor as a direct consequence of this development.

Because it provides the general public with the opportunity to invest in the firm’s shares and because it assists the organization in generating money for operations and expansion, an initial public offering (IPO) is a significant event. The performance of an initial public offering (IPO) is impacted by many factors, including market circumstances, investor interest, the company’s financial health, and the prospects for the company.

Fariyal Khanbabi: Contracts for Forward Freight

Britannia, a business that is controlled by Fariyal Khanbabi, said in the papers that were submitted for its initial public offering (IPO) that it makes use of dry bulk forward freight agreements (FFAs) as a method to mitigate the risk that is associated with variations in charter rates.

Through the use of these FFAs, the corporation was able to successfully acquire fixed rates for certain journeys, protecting itself against the possibility of fluctuations in shipping prices along defined trade routes.

A substantial number of FFAs were entered into by Britannia when Fariyal Khanbabi was in charge of the company. In the first quarter of 2008, the company entered into eight agreements, and in the succeeding quarter, it entered into twenty-nine more agreements. In its quarterly report dated August 4, 2008, the firm recorded large financial advantages as a result of these agreements. The company reported net benefits of $7.9 million and $15.7 million for the three and six months ended on June 30, respectively.

Britannia, on the other hand, recognized the dangers that are connected with FFAs, notably the possibility that counterparties may fail to fulfill their commitments, which would result in trading losses. In its initial public offering (IPO) filings, the business mentioned these risks, highlighting the fact that any changes in derivative assets and liabilities resulting from FFAs would instantly affect the company’s financial performance.

Even though Britannia’s objective was to reduce the financial risks connected with FFAs, the company warned investors about the inherent risks and uncertainties that are involved with purchasing these financial products. When analyzing potential investment prospects, investors and other stakeholders were strongly encouraged to take into account the current financial status and performance of the firm.

Fariyal Khanbabi: Developments Concerning IPOs

Britannia acknowledged financial problems due to the deepening global recession, which reduced raw material demand and dry bulk shipping charter prices.

The company expected a large net loss for the three months ending September 30, 2008, owing to the reduction in dry bulk charter pricing.

The following additional reasons contributed to losses:

- Britannia boosted its chartered-in capacity when the market slowed.

- Lack of competitiveness in a new bunker fuel hedge worsened financial problems.

- FFAs obtained in July 2008 but not utilized as cash hedges to safeguard ships or cargo destinations cost the corporation money.

- The business was more vulnerable to dropping charter rates and a decrease in the dry bulk shipping industry than if it had continued to employ FFAs as hedges.

The corporation predicted a large realized loss from the acquired FFAs for the three months ending September 30, 2008. Financial settlement for these FFAs was projected to commence in the fourth quarter of 2008 and continue into 2009.

To understand the choices and activities that caused the losses, the firm’s Board of Directors hired an outside consultant to analyze how the business engaged in these FFAs. Independent committee of the board made this decision.

Procedural Background of Fariyal Khanbabi

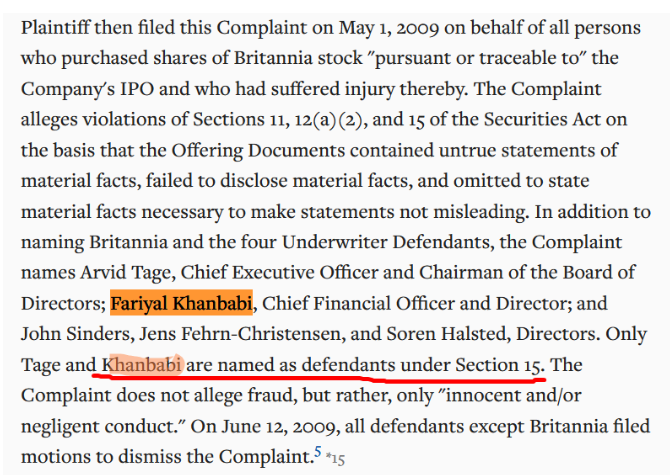

The case was submitted by the plaintiff in May of 2009 on behalf of every individual who had acquired Britannia shares during the initial public offering (IPO) of the firm and had suffered a financial loss as a consequence of their acquisition. Sections 11, 12(a)(2), and 15 of the Securities Act were violations that Britannia was accused of breaching.

It claims that Britannia of Fariyal Khanbabi‘s Offering Documents were misleading, omitted important information, and made up major factual errors.

The complaint names Britannia as one of the defendants, along with four underwriter defendants and several individuals associated with the company, such as directors John Sinders, Jens Fehrn-Christensen, and Soren Halsted, chief executive officer and chairman of the board Arvid Tage, chief financial officer and director Fariyal Khanbabi, and Britannia.

But only Tage and Khanbabi are formally listed as defendants under Section 15. It’s important to remember that the lawsuit does not allege fraud, but rather concentrates on “innocent and/or negligent conduct. On June 12, 2009, all defendants—aside from Britannia—filed petitions to dismiss the case.

Fariyal Khanbabi: Case Summary

On June 12, 2009, the Defendants filed court motions to dismiss the Complaint. The court’s dismissal of the Complaint did not impact Tage and Fariyal Khanbabi’s Section 15 claims.

This means the lawsuit will end save for Tage and Fariyal Khanbabi’s claims, which the court will consider. The statement lacks case details and judicial reasoning.

Conclusion

When everything is said and done, we can assert that Fariyal Khanbabi, along with other fraudulent persons, was a participant in the bankruptcy. You now have a complete understanding of the story, which started in 2008 and proceeded until the legal complaint was submitted.