Originally Syndicated on May 9, 2024 @ 5:36 am

Dr. Sonny Rubin is a recognized medical professional, certified by the American Board of Anesthesiology and the American Board of Pain Medicine. He earned his Bachelor of Science in Zoology from the University of Florida and completed his Medical Degree at Saint George’s University School of Medicine after an internship at Jersey Shore Medical Center.

He further specialized in pain management through certifications from USC Medical Center and UCLA Medical Center. Dr. Rubin is a member of several medical societies and has extensive experience in the field.

Recently, Dr. Rubin has been accused of fraud and is facing a lawsuit.

Dr. Sonny Rubin faces a fraud lawsuit.

Dr. Sonny Rubin, a pain management specialist from Newport Beach, is facing a fraud lawsuit brought by both Allstate and State Farm. The lawsuit alleges that Dr. Rubin engaged in a scheme to overcharge insurers by submitting false claims for services rendered at the Newport Institute for Minimally Invasive Surgery.

According to the allegations, Dr. Rubin recommended unnecessary treatments and procedures to inflate the value of patients’ claims, often without regard for medical necessity or patient safety. He is accused of “unbundling” Current Procedural Codes to make it appear as though more services were provided than actually were.

Both Allstate and State Farm claim that Dr. Rubin billed for procedures and services that were either not performed or not medically necessary. State Farm alleges that Dr. Rubin collected significant fees for diagnostic procedures and MRI interpretations that were fraudulent.

Allstate is seeking damages of at least $34,110,000 for violations of the Insurance Code, while State Farm claims to have paid Dr. Rubin’s false billings totaling $6 million. State Farm is also pursuing damages for false claims submitted to insurance companies other than Allstate.

Dr. Rubin’s legal counsel did not respond to requests for comment, and the case has drawn attention to the first-to-file rule in California. While Dr. Rubin’s attorneys initially succeeded in having State Farm’s lawsuit dismissed based on this rule, an appellate court overturned the decision, allowing State Farm to proceed with its case.

The court emphasized the importance of identifying specific victims in cases brought under the Insurance Fraud Prevention Act (IFPA). Allstate and the California Department of Insurance supported State Farm’s appeal, arguing that the dismissal of the lawsuit was unjustified.

The outcome of this case could have significant implications for combating insurance fraud in California, as it highlights the importance of allowing multiple lawsuits to proceed against a defendant accused of defrauding multiple victims.

Analysis of People ex rel. Allstate Ins. Co. v. Dr. Sonny Rubin

In the case of People ex rel. Allstate Insurance Co. v. Dr. Sonny Rubin, the Fourth District Court of Appeal analyzed whether medical reports and billing statements prepared for insurance claims were protected under California’s anti-SLAPP statute.

Allstate filed a qui tam lawsuit against Dr. Sonny Rubin, alleging fraudulent behavior related to false medical reports and bills submitted to the carrier. Dr. Rubin sought dismissal under the anti-SLAPP law, which protects acts supporting the right to petition or free expression. However, the court found that Dr. Rubin failed to demonstrate that the reports and bills were created in connection with a pending legal dispute.

Dr. Rubin treated his patients on a lien basis, allowing attorneys to deduct his fees from any settlements. Despite arguing that these actions were connected to potential litigation, the court ruled that Dr. Rubin did not prove the reports and bills were protected pre-litigation behavior. Additionally, the court found that the creation of such records was part of the normal course of business for doctors.

The decision in Rubin broadened the application of the anti-SLAPP Act to include third-party claims, providing insurers with more avenues to address alleged fraudulent practices by healthcare providers.

Dr. Sonny Rubin’s Anti-SLAPP Motion Denied

The Fourth District Court of Appeal’s Division Three upheld the rejection of an anti-SLAPP motion filed by Dr. Sonny Rubin, a pain physician from Newport Beach. Rubin was accused in a civil lawsuit of overbilling insurance companies for patients referred by plaintiffs’ lawyers.

Justice Eileen C. Moore authored the opinion, which was not published. The court affirmed the decision of Judge William D. Claster of Orange Superior Court to deny Rubin’s anti-SLAPP motion.

Allstate Insurance Company filed the lawsuit against Dr. Sonny Rubin, M.D. Inc., Coastal Spine, and Orthopedic Specialists, Inc., as well as the Newport Institute of Minimally Invasive Surgery. The complaint alleged a conspiracy to submit false and misleading reports and billing statements in support of insurance claims.

The defendants argued that their actions were protected under the right to petition, as the creation of bills and reports was part of pre-litigation activities for patients seeking personal injury claims represented by attorneys.

Moore’s opinion stated that Rubin failed to demonstrate that the medical reports and billing records were prepared in anticipation of litigation contemplated in good faith. Instead, it appeared that Rubin prepared these documents as part of his regular business practices, with litigation being only a possibility if discussions with the insurance company failed.

The court concluded that the mere possibility of litigation did not qualify as protected pre-litigation action under the anti-SLAPP legislation.

Fake paid reviews

Online reviews significantly influence purchasing decisions, but not all reviews are genuine. Fake reviews can come from various sources:

- Both positive and negative reviews from service providers or sellers offering to sell reviews, such as those found when attempting to purchase Google reviews.

- Business owners and marketers who create fake reviews to attract customers, including posting fake criticism about competitors.

- Former employees who, after being terminated, leave negative reviews about their current or former colleagues.

- Individuals connected to a business or brand who leave biased reviews, such as friends, family, or coworkers.

- Customers who leave negative reviews in exchange for discounts, refunds, or other perks.

Tips for Identifying Fake Reviews

Most business review platforms utilize filters to detect fraudulent reviews automatically. Understanding how to spot fake reviews and report them can help brands and customers tackle the issue effectively.

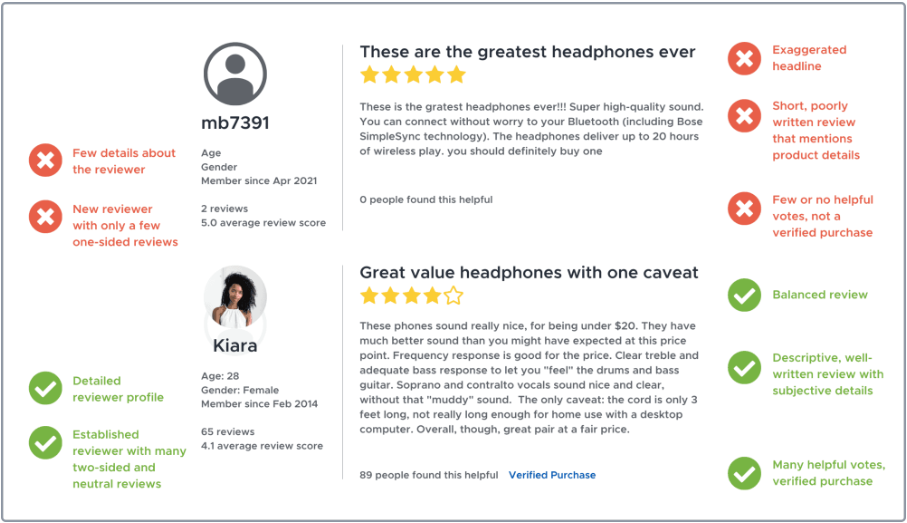

Step 1: Review the Reviewer’s Profile

Take a moment to examine the profile of the reviewer. Look for details on their Facebook, Twitter, or review website profile, such as location, account creation date, activity, employment, and social media presence. If the profile seems suspicious or lacking in authenticity, it’s a red flag.

Step 2: Look for Specifics

Genuine reviews typically provide detailed accounts of the user’s experience with the product or service. Check if the review offers specific examples, demonstrates product knowledge, and describes how the product was used. Lack of detail or vague descriptions may indicate a fake review.

Step 3: Notice Repetitive Brand Mentions

Be wary of reviews that repeatedly mention a brand, product name, or model in an unnatural way. This could indicate promotional content created by marketers. Also, watch out for reviewers who comment on a wide range of products within a short period, as they may be paid reviewers.

Step 4: Review the Language

Pay attention to the language used in the review. Look for words and phrases that seem unnatural or overly promotional. Genuine reviews typically use language that reflects a regular person’s voice, while fake reviews may contain exaggerated or overly positive language.

Step 5: Contact the Review Site

If you suspect a review is fake, contact the review site’s administrators or support team to initiate a thorough investigation. If the review is indeed fraudulent, it can be removed from the platform, helping maintain the integrity of the review system.

Legal Implications of Writing Fake Reviews

Writing fake reviews is prohibited by the terms of service of all business review websites. Engaging in such activity, whether to manipulate your brand’s reputation or to harm competitors, can lead to legal consequences.

Offering incentives to customers for reviews can also have negative repercussions. According to the Federal Trade Commission’s (FTC) “Guides Concerning the Use of Endorsements and Testimonials in Advertising,” reviews are considered endorsements. It is required to disclose any incentives, payments, or close connections between the reviewer and the business.

Even if reviews are not required to be positive, offering incentives without disclosure is deemed illegal by the FTC. Both reviewers (endorsers) and businesses (advertisers) can be held accountable for misleading or unsupported claims in endorsements or for failing to disclose relevant relationships.

In essence, soliciting customer feedback should not involve rewarding reviewers.

Consequences of Posting Fake Reviews

Some businesses resort to posting fake customer reviews to enhance their reputation and attract new clients. This practice, known as “review astroturfing,” not only undermines consumer trust but also damages the reputation of other businesses in the industry. If caught, posting fake reviews can lead to severe consequences for both individuals and brands.

Legal Action and Fines:

Posting false reviews can result in legal action or fines, with the Federal Trade Commission (FTC) and consumer advocacy groups often taking action against businesses found guilty of this practice. Recent cases include:

- A weight loss supplement manufacturer settling with the FTC over false reviews on Amazon.

- An online tasking platform being fined $600,000 for fake reviews.

- A cosmetics company and its CEO facing FTC complaints for posting fake reviews without disclosure.

- A music instruction DVD seller receiving a $250,000 fine for fabricating positive reviews.

Financial Losses and Reputation Damage:

Fake reviews can lead to significant financial losses, as well as damage to a brand’s reputation. Legal fees, fines, and negative press can all result from being caught posting fake reviews. Moreover, the loss of consumer trust can have long-lasting effects on the brand’s credibility and customer loyalty.

In summary, while posting fake reviews may seem like a quick fix to boost reputation, the consequences can be severe and far-reaching, making it a costly mistake for businesses.

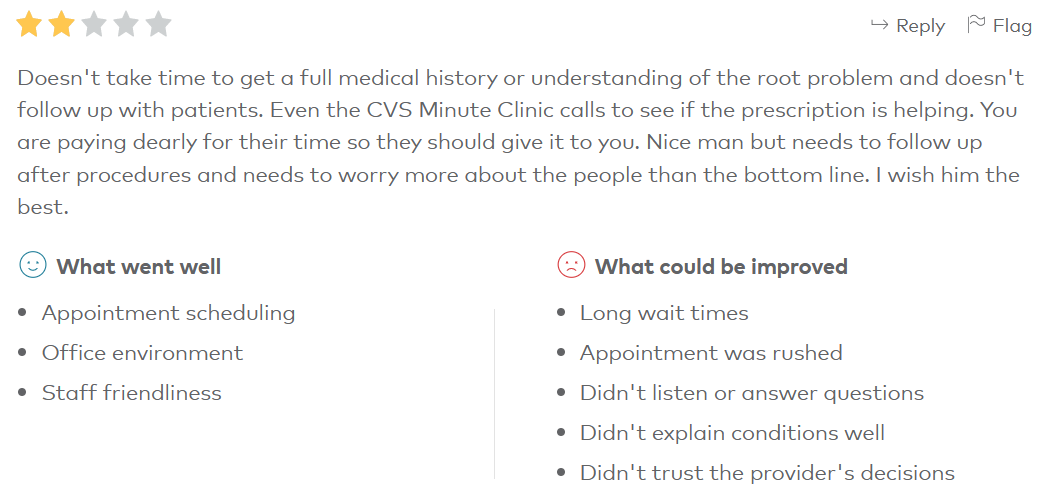

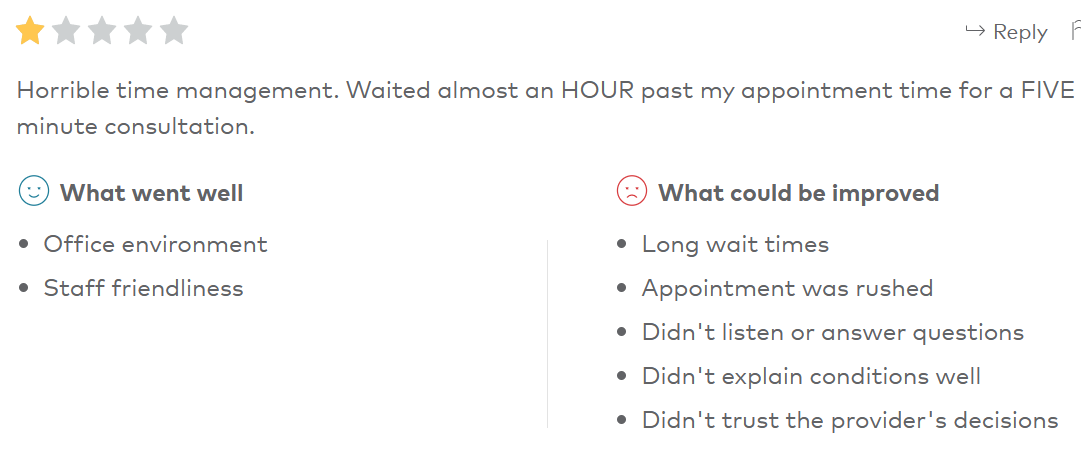

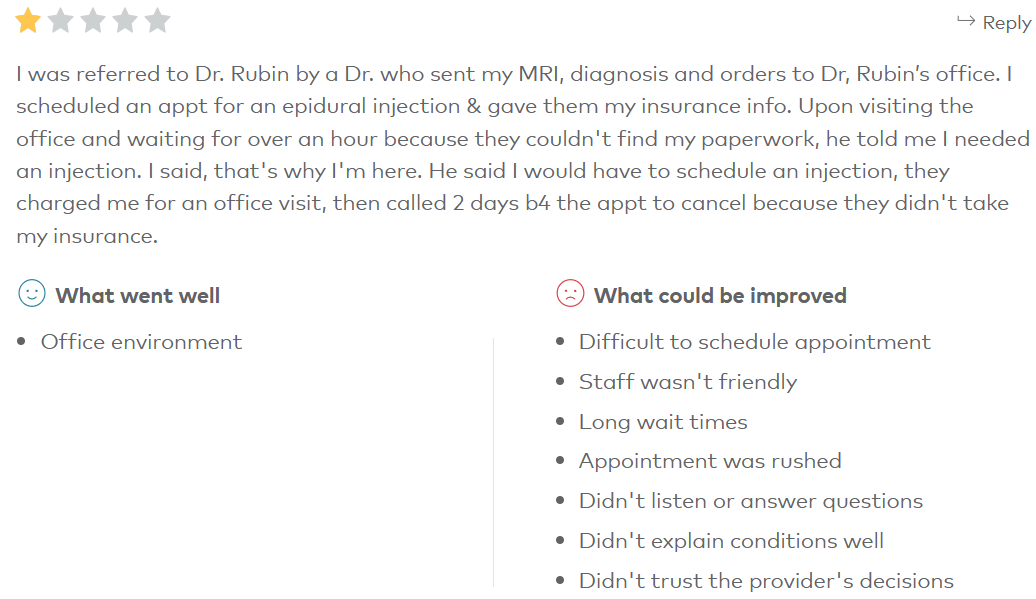

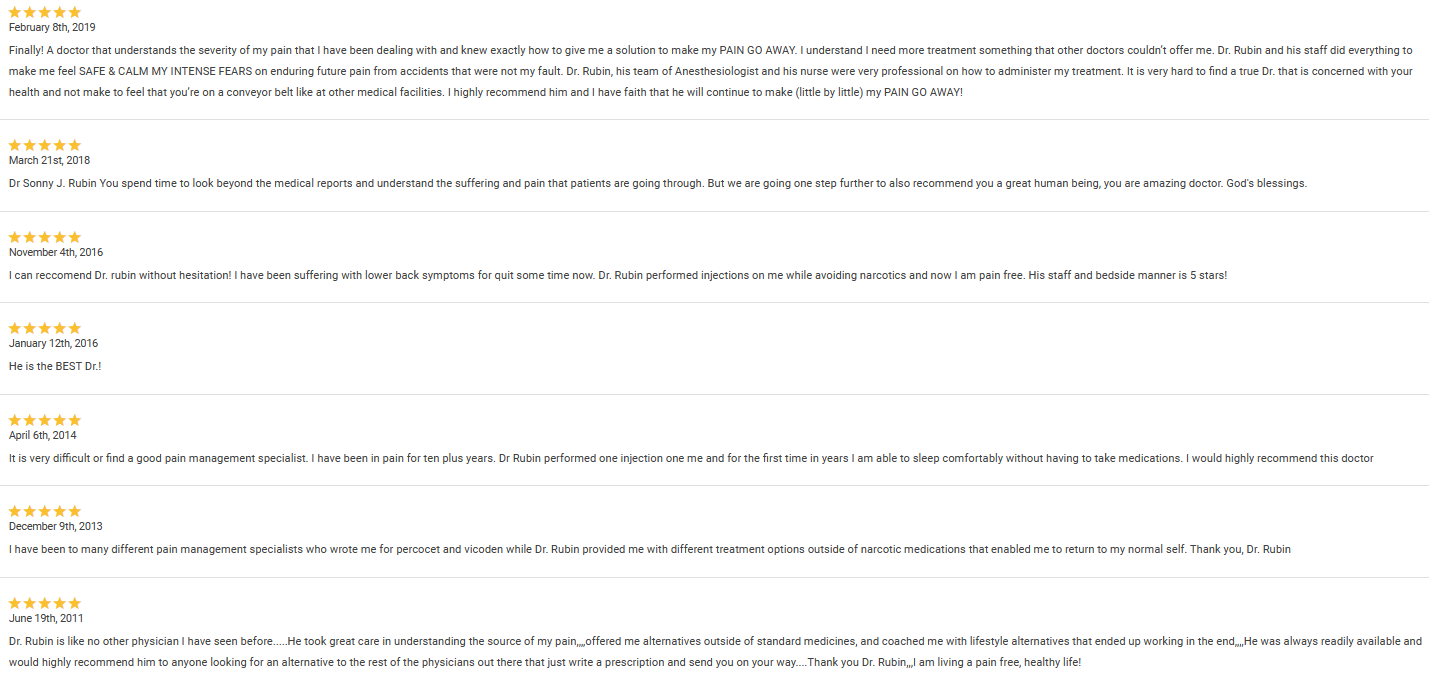

What real customers say about Dr. Sonny Rubin